M&A deals in 2022: analysing the tax risks and identifying the challenges of a business can define the success of a deal

17 March 2022

- The due diligence analysis is one of the most important steps in a transaction

- The number of tax audits had an increasing trend in the last years

- The ongoing tax litigations, alongside the eligibility of tax reliefs and the open periods for tax audits, are among the most common tax areas in a share-deal transaction

Despite concerns about COVID-19, resurgent inflation, and rising energy prices, 2021 saw robust dealmaking across the CEE region. As we have noted in a recent article regarding the maturity of the M&A market, in 2021 there were 49 disclosed deals[1] among Romanian companies, which means an increase of 17% compared to the previous year. Thus, we note that, after 2 years since the global economy was affected, the interest of strategic investors and investment funds remains relevant at the local level as well.

From an industry perspective, last year was a very active one for Energy companies (7 deals), Software companies (7 deals), and Financial services companies (also 5 deals), with the energy sector also benefitting from the largest deal of the year (Neptun Deep Block concession).

We don’t know yet what 2022 will bring, but what we know for sure is that the investors or financial companies, that are planning transactions for this year, need to consider several tax issues, regardless of how the deal is intended to be performed or its stage. Thus, a process of due diligence, carried out prior to the deal signing, is more than recommended. This kind of analysis facilitates the investment decision-making process and, at the same time, provides the latter with future protection against potential identified risks.

We will further analyse the implications of a transaction in the form of a share deal.

„First of all, we consider it important for the investor to know how the company in which it intends to invest has operated up until the time of the acquisition, from a legal, commercial, financial, tax, and human resources perspective. Secondly, in relation to tax issues, a tax due diligence exercise carried out before the transaction, will enable the investor to know the tax status of the company in which it intends to invest (for example, whether or not it has been subject to tax inspections during the statute of limitation period), to identify the areas with potential tax risk, so that in the end, these areas are quantifiable and adjustable through the mechanism for setting and paying the price related to the transaction.”, mentioned Lucian Dumitru, Tax Director, Mazars Romania.

The importance of tax issues in the decision-making process

Considering the tax measures adopted in the context of the COVID-19 pandemic by the Romanian authorities, we mention that the aspects of this nature are even more pressing in establishing the tax clauses in the Sale-Purchase Agreements.

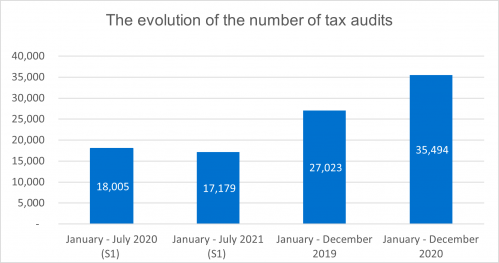

„Moreover, according to the annual performance reports[2] of the National Agency for Fiscal Administration (NAFA), we observe an upward trend in the number of tax inspections, respectively an annual increase of almost 30% in 2020 compared to 2019, while in the first half of 2021 we observe that the number of tax inspections has remained stable, referring to the same period of 2020.”, mentioned Andreea Ignătescu, Tax Manager, Mazars Romania.

Source: Activity report of NAFA, available on their website

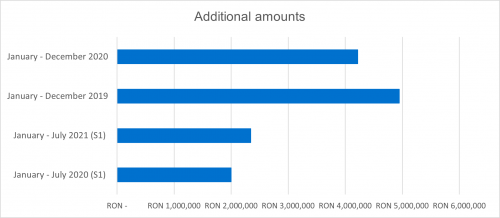

At the same time, we notice an upward trend of the amounts additionally established following the tax inspections carried out in the first half of 2021, compared to the same period of the previous year:

Source: Latest available data, issued by NAFA

Therefore, these trends support the idea that, prior to any such transaction, the tax risks must be known, and a due diligence exercise is important to manage those coming from past periods, taken over with the completion of the transaction.

Key focus tax areas and challenges in acquisition structures

Investors can use a number of mechanisms to ensure their protection against potential tax risks that may materialise in a share deal, such as negotiating specific terms, introducing safeguards, and adjusting the transaction price.

Some of the most common tax risks in a share-deal transaction are:

- Open periods for tax audits - the history of tax inspections and audits is an area that needs to be carefully considered. A clear visibility of the open periods for tax audits provides the investor with protection against tax risks that may materialise after the acquisition. The history of the tax inspections should also be analysed from the perspective of the risk areas reported by the inspectors and the degree of subsequent compliance of the company that the investment is made in. In the absence of measures to correct and rectify the elements that led to the issues identified in a completed tax audit, it is not excluded that the same risk areas may be subject to a future tax audit.

- Ongoing tax litigation - the area of ongoing tax disputes and litigation, that is happening at the same time with the due diligence analysis may influence the investor's decision on whether or not to complete the transaction. Given their complexity, the settlement process can be extended over a long period, implicitly and after the completion of the transaction. In such cases, the investor must be aware in advance of the issues which are the subject of the litigation, of the risks to which it is exposed with the acquisition of the company, and of the degree of materialisation.

- Eligibility of tax reliefs - the application of tax reliefs is frequently an area of close scrutiny in tax audits, given the tax impact that they may have. Among the most common reliefs, we mention the income tax exemption for IT activities, R&D reliefs, and corporate income tax exemption for reinvested profits. Also, the tax facilities and benefits introduced during the COVID-19 pandemic, such as tax payment bonuses, instalments and deferrals for tax liabilities, technical unemployment benefits for temporary suspensions of employment in the context of COVID-19, and others are becoming increasingly relevant for inspectors. Non-compliance with the tax provisions may lead to the loss of eligibility for the application of these facilities, and thus to potential additional taxes following the transaction.

- Potential reclassifications in the area of payroll taxes - among the most important issues, we mention the analysis of the activities carried out by self-employed individuals for the benefit of the acquired company (under the risk of reclassification of activities from self-employed to dependent, which may generate additional payment obligations in the area of payroll taxes and social contributions), investigation of new working patterns for employees (either hybrid or under the transition from employee to self-employed status or the establishment of a limited liability company, etc.). These cases have an increased frequency depending on the industry, particularly identifiable in the area of IT services, medical/clinical services.

„It should be noted that, beyond the fulfillment of the formal requirements, the tax authorities pay more attention to the substance of the transaction and how such persons actually carry out their activities for the company invested in. Also, according to the legal provisions, the tax authorities may reclassify such transactions so that they reflect the economic content, the latter prevailing over formal aspects.”, mentioned Elena Dima, Tax Senior Consultant, Mazars Romania.

- The transactions with related parties, in terms of the market price documentation, continue to be under constant scrutiny by the tax authorities. In 2020, according to the same performance report prepared by the tax authorities, the additional tax liabilities established as a result of transfer pricing inspections almost doubled compared to 2019. The difficulties can translate into significant costs and efforts after the acquisition process if the company to be acquired does not have a complete and compliant documentation, as per the local tax legislation. Furthermore, there may be practical difficulties for the investor to access or obtain past information for the transactions with related parties, which makes the process of preparing the said documentation more challenging. Based on these considerations, it is recommended that the process of preparing the transfer pricing documentation for the pre-transaction periods to remain the responsibility of the seller. Alternatively, such responsibility of the seller should be included as a separate clause in the Sale-Purchase Agreement, to be carried out post-closing of the transaction.

- The deductibility of service expenses and how these expenses are documented remains an ongoing area of interest for tax inspectors, especially for the acquisition of services from affiliated group entities. Similar to the transfer pricing documentation, the process of obtaining supporting documentation for service acquisitions made from group companies, for periods prior to the transaction, can be equally laborious and involves additional resources from the investor. Therefore, the recommendation is to provide them in advance by the seller, as part of the transaction, in order to ensure comfort for potential tax risks in the area of tax deductibility (for corporate and VAT purposes).

Also, many other tax areas may be of increased interest to the tax authorities, depending on the specifics of the business and sector in which the company invested in operates. It is therefore recommended that prior identification of these issues, together with their quantification and negotiation in the transaction price, should not be missing from the buyer's investment process.

Regardless of the size of the company invested in or the industry in which it operates, the tax issues and how they are addressed in the context of the transaction will frequently be of interest, with a significant impact on the terms and price of the transaction, as well as the inherited tax risks.

###

Contact

Emilia Popa, Head of Marketing and Communication, Mazars Romania

emilia.popa@mazars.ro / +40 741 111 042

About Mazars

Mazars is an internationally integrated partnership, specialising in audit, accountancy, advisory, tax, and legal services*. Operating in over 90 countries and territories around the world, we draw on the expertise of more than 44,000 professionals – 28,000+ in Mazars’ integrated partnership and 16,000+ via the Mazars North America Alliance – to assist clients of all sizes at every stage in their development.

*where permitted under applicable country laws.

www.mazars.com | Mazars on LinkedIn

About Mazars in Romania

In Romania, Mazars has 27 years of experience in audit, tax, financial advisory, outsourcing, and consulting. Our strength lies in the people we work with – the local team has 7 partners and 280 professionals.

www.mazars.ro | Mazars Romania on LinkedIn

[1] according to the Mergermarket and Mazars Inbound M&A report 2021/2022.

[2]https://www.anaf.ro/anaf/internet/ANAF/despre_anaf/strategii_anaf/rapoarte_studii

Contact